》View SMM Silicon Product Prices

》Subscribe to View Historical Price Trends of SMM Metal Spot Cargo

Reviewing the price trends of raw materials across various segments on the cost side of silicon metal in 2024, it can be observed that raw material costs experienced varying degrees of decline, which in turn drove silicon metal costs downward. However, constrained by the persistent surplus in the silicon metal market in 2024, silicon prices fell rapidly. The decline in raw material costs was far less than the drop in silicon prices, resulting in poor overall profitability for the industry in 2024, with most silicon enterprises entering loss-making production stages early on.

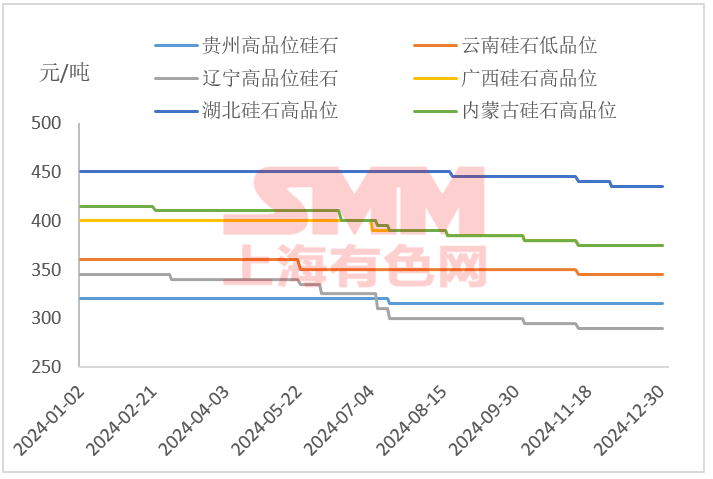

Currently, the five main raw materials for silicon metal are silica, silicon coal, electrodes, charcoal, and petroleum coke. For silica, a necessary raw material for silicon metal smelting, prices in various regions saw varying degrees of decline this year. Even in Hubei, where demand remained consistently high, silica prices in 2024 also showed a certain degree of decline. However, the price drop in the silica segment has been relatively small, and with the increasing number of self-supplied mines by downstream silicon enterprises in 2024, the supply side of silica remains ample. Compared to the price declines of other silicon metal raw materials and silicon metal itself, there may still be some downside room for silica prices.

Currently, due to differences in industrial choices, silicon metal enterprises use varying combinations of raw materials in production and smelting. Downstream silicon metal smelting mainly employs three technologies: all-coal process, coal-coke process, and charcoal process. Different processes use different reducing agents. The main reducing agents—silicon coal, petroleum coke, and charcoal—vary in value, and factors such as transportation costs also contribute to certain price differences in costs among the processes.

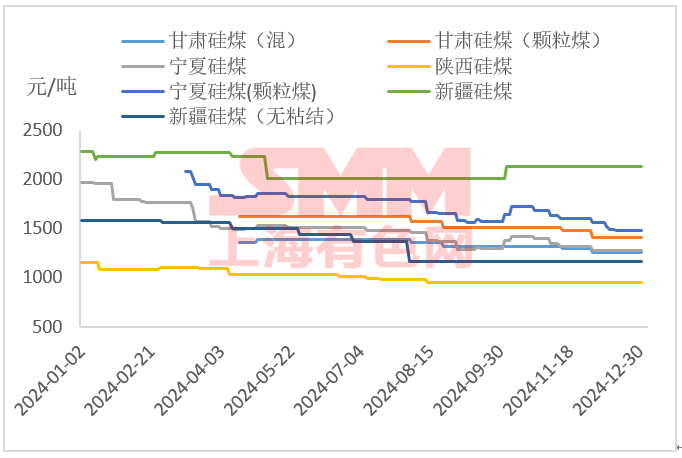

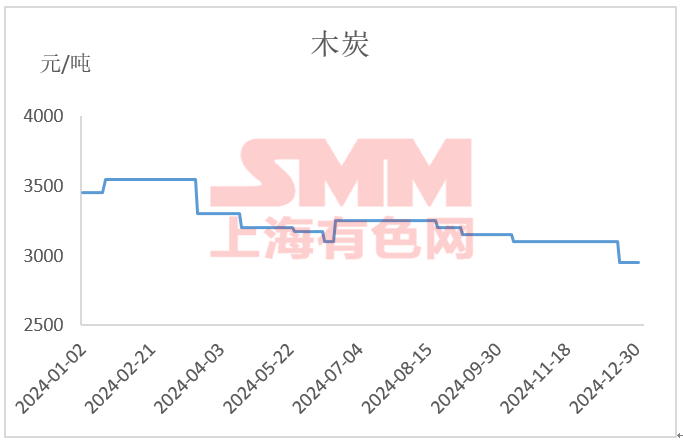

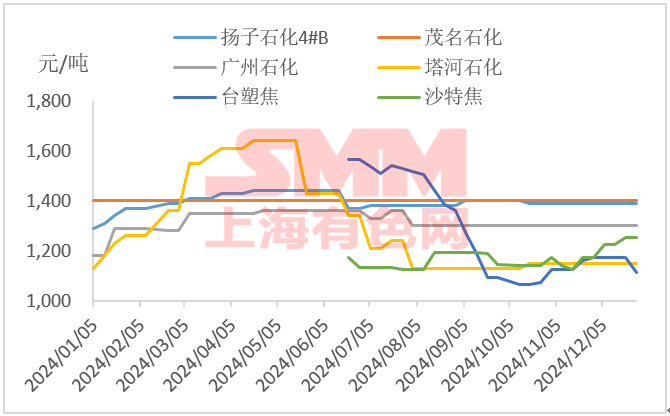

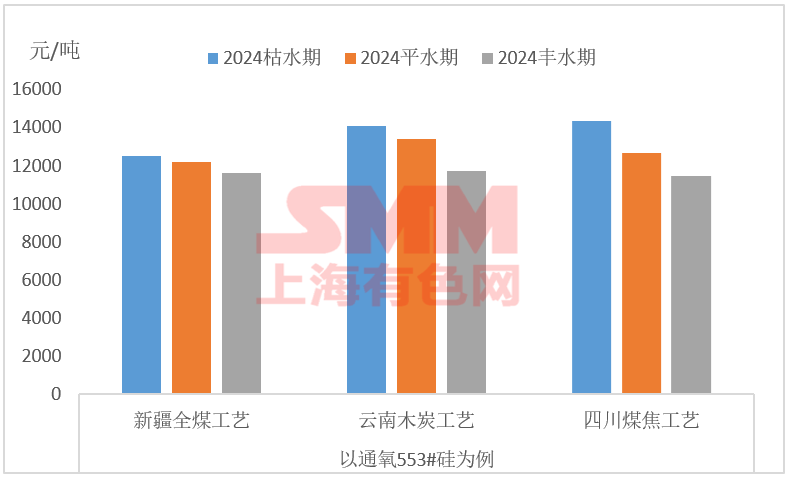

In terms of carbon-based reducing agents, prices in 2024 generally declined, except for petroleum coke, which fluctuated. Among them, the largest decline was in the silicon coal segment. Silicon coal prices, being relatively low among the three major reducing agents, combined with a continuous decline throughout 2024, significantly reduced costs for all-coal process manufacturers. Charcoal, due to its already high price and limited price decline in 2024, saw only moderate cost reductions in the charcoal process. Petroleum coke, benefiting from its low price and frequent mixing with silicon coal, also contributed to some cost reductions in the coal-coke process. Taking above-standard #553 silicon metal from the three major production regions—Xinjiang, Yunnan, and Sichuan—as examples, cost calculations were conducted based on different processes in different regions.

Although the smelting costs of all three processes declined in 2024, as mentioned earlier, the rapid drop in silicon prices far outpaced the decline in costs. As a result, average industry profits remained minimal, with most silicon enterprises entering loss-making stages early on. In 2024, manufacturers faced significant production pressure, with operating rates dropping sharply from Q4. Looking back over the year, production pressure on silicon metal manufacturers continued to rise. Despite cost reductions across all three processes, profitability remained elusive.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)